Irregular: The geopolitics of losing money

How to avoid being blindsided by political turmoil.

Hello from Sydney,

In this week’s Irregular column, I explore how geopolitics affects markets – and how closely tracking international political developments can not only insulate investment portfolios but help the savvy get an edge. And for our GD Pro subscribers who couldn’t make our most recent monthly webinar, I’ve included a recording at the end of this email.

Bear Hugging, Bear Market

Geopolitics is now top-of-mind for investors. A recent PGIM survey found that 56% of institutional investors believe the threat level from geopolitical risk is high, while 59% say it is actively harming portfolio outcomes. Similarly, BCG’s 2024 Global Investor Survey found that 51% of investors rank geopolitics as a top-three risk—a bigger concern than interest rates or inflation and a 15-point increase from the previous year.

Even Australia’s sovereign wealth fund now calls geopolitics “the bedrock of the new investment order.”

For investors who still aren’t convinced, this past week may have changed their minds.

On Monday, the S&P 500 plunged, Treasury yields pulled back, and the Nasdaq suffered its worst day since 2022, falling 4.3%. Nvidia, the tech index’s former start, is now down 20% year-to-date. Tesla, on the same timescale, is down 41.4%.

This turmoil comes as no surprise given the political volatility of the past six weeks. Since returning to office, Donald Trump has reversed US support for Ukraine, opened peace talks with Russia, introduced aggressive new tariffs, and created tremendous uncertainty about the future of the US public service, financial regulation, and the transatlantic alliance. More broadly, the US is signaling a retreat from its traditional post-WWII role as global economic stabiliser.

And there’s new uncertainty developing far beyond the United States. In Europe, existential angst has led to a surge in defence spending, tensions have revived in the Balkans, and Germany has elected a new government (which then lifted the hitherto sacrosanct debt ceiling). In the Middle East, new threats and back channels have emerged in Gaza, Iran has been offered a seeming choice between nuclear dialogue and nuclear brinksmanship, and Syria’s new government has faced the threat of an Alawite insurgency. And elsewhere, the Philippines is facing a constitutional crisis, South Korea is embroiled in one, and the threat of a civil war is brewing in South Sudan.

And that’s just the tip of the iceberg. (For a full breakdown of global events and their market impacts, subscribe to the paid version of Geopolitical Dispatch.)

Bonds, James Bonds

Markets move for many reasons, just as people act for many reasons. But the data now clearly shows that geopolitics is playing a more significant role in trading activity than ever before.

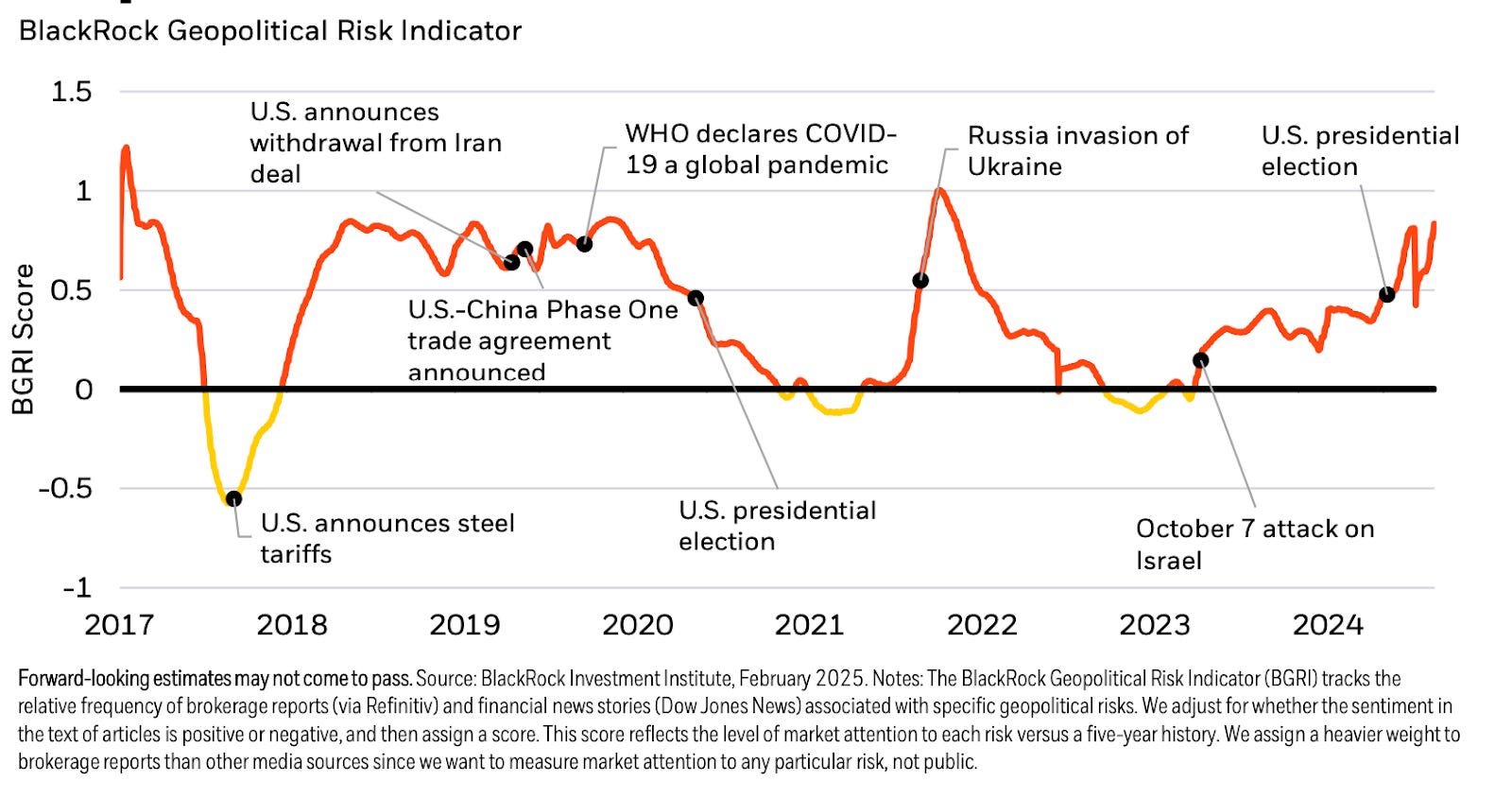

Perhaps the best measure of this is the BlackRock Geopolitical Risk Indicator, which tracks brokerage and financial media mentions of ten major geopolitical risks—measuring both frequency and sentiment. The latest report, published on 21 February, shows a clear uptick in market attention to geopolitics.

Not all risks are created equal, however. Some risks—such as tensions in the Middle East, North Korea, or Russia-NATO relations—have remained relatively stable since Trump’s re-election.

But others have spiked dramatically:

Global trade protectionism

US-China strategic competition

European political fragmentation

Major cyber or terror attacks

Emerging markets political crises

Unsurprisingly, markets are especially jittery about the risk that, in BlackRock’s definition, “tariffs will increase dramatically on goods entering the United States, negatively impacting the macro outlook.”

Does this mean this week’s sell-off was purely about geopolitics? Not necessarily. But most analysts attribute it to Trump’s erratic trade, foreign, and economic policies—all of which are geopolitically driven and will have long-term geopolitical consequences.

The Intelligent Investor

Despite the overwhelming evidence, some investors still dismiss geopolitics as unpredictable “noise” that can’t be integrated into investment decisions.

Some argue that historically, there’s been little long-term correlation between geopolitical risk indices and stock market returns—that fundamentals ultimately prevail over time. Others believe it’s too complex to integrate into models, given the lack of structured data. And many assume that geopolitical risks are already priced in—that by the time an investor reacts to a global event, it’s too late to gain an edge.

These arguments are not entirely wrong. But they miss the bigger picture.

In Good Company

Geopolitics affects the fundamentals of asset valuation—often in ways traditional financial models fail to capture.

Risk premiums can spike due to political uncertainty, sanctions, tariffs, or wars. Inflation can surge due to supply chain disruptions—just as Russia’s invasion of Ukraine sent food and energy prices soaring. And tax incentives, subsidies, and trade restrictions can dramatically alter cash flows for entire sectors. Just ask American importers now scrambling to predict the next round of Trump tariffs—or whether they’ll be able to pass costs onto consumers.

Having a grasp of the geopolitical factors behind government policies can therefore provide a significant edge in more accurately pricing financial assets —whether bonds, stocks, real estate, private equity or infrastructure — by determining if they are under- or over-valued, and getting ahead of markets

Beyond affecting asset valuation fundamentals, geopolitical events often have a pronounced impact on a particular industry or sector that may unwittingly become swords or shields in geopolitical combat.

Over the past few years, US-China tensions have seen their respective governments identify and protect what they see as “strategic sectors” – whether semiconductors, raw materials, critical minerals, advanced technologies or defence industries. This trend has only accelerated under the new Trump Administration, which not only has levelled new tariffs on China and got some back in return but has talked of annexing Canada and Greenland and forcing Ukraine to capitulate, all while eyeing off each country’s critical minerals.

Understanding these states’ national security proccupations, as well as the idiosyncratic motivations of leaders, can provide insights into what industries are likely to be supported through measures like subsidies and tax breaks, become the target for offensive measures like sanctions and trade restrictions, and/or are likely to grow through greater demand from government procurement.

An even cursory look at major governments’ national security priorities, projected defence spending and the (rapidly) evolving lists of allies and marriages of convenience can help investors identify industries and sectors worth investing in. But in a rapidly changing global environment, with shifting political allegiances and greater geopolitical uncertainty, affected industries are constantly changing.

Similarly, geopolitical events can damage some industries but benefit others. A terrorist attack, for instance, often leads to sustained losses in travel and insurance while defence, pharmaceuticals and commodities often do better. Keeping on top of changes through close monitoring of geopolitical events is therefore vital to identify what to buy and sell, and when.

It’s the Economy, Stupid

Geopolitical disruptions can have economy-wide impacts, as the United States may well be experiencing right now. The data shows that an outbreak of armed conflict or a terrorist attack often has significant, albeit short-lived, impacts on overall sentiment. But the mere anticipation of conflict can seriously affect financial assets – by depressing stock markets, driving down government bond yields, and lifting gold and oil prices. While few are expecting new hot wars to break out any time soon, the anticipation of a global trade war appears to be having a similar effect.

Rivalries and tensions between major energy and commodities producers can also have major economic impacts. Russia’s invasion of Ukraine and the subsequent imposition of Western sanctions and turning of Russian exports towards Asia (including oil at a discount) not only affected the value of Russian companies and the overall performance of Russian industry, but also significantly affected global oil and commodity prices, with a wide range of consequences. And, by contrast, in the past few weeks, the Russian ruble and stocks have surged following phone calls between Trump and Putin, and whisperings of US sanctions relief.

Geopolitics also moves currencies. Oil shocks, for instance, tend to benefit oil-exporting countries as against the US dollar and oil-importing countries’ currencies. Major stimulus and investment programmes in advanced economies driven by geopolitics can move currencies as well – whether inadvertently or by design.

The Bedrock

Finally, at a more structural level, the whole question of a shifting world order has direct financial impacts. The dominance of the US dollar as the world’s reserve currency is owed in no small part to the United States becoming the preeminent superpower after the Second World War and creating an international financial architecture supporting its hegemony.

The institutions created over the past 80 years – the World Bank, the International Monetary Fund, the World Trade Organization, the United Nations, and a thicket of preferential trade agreements – have supported a historically anomalous period of peace and prosperity.

But these institutions are creaking, and the United States, under Trump, appears to be walking away from its traditional leadership role and support for these institutions and the broader “rules-based order”. As the world becomes more multipolar and the institutions and rules of engagement in international affairs more closely resemble the actual distribution of power, we may find the foundations of the international system upon which the global trade and financial system rest suddenly feel more shaky.

A Professional Approach

In short, geopolitics moves markets. It affects valuations in the short-term and the long-term, at the micro- and the macro- levels, and in some ways is the foundation of the global economy. Investors ignore it at their peril.

That does not mean being jumpy or reactive or prioritising geopolitics over other market fundamentals. It does, however, mean knowing what matters, what doesn’t, and when to act. It requires cutting through the noise, monitoring daily events without losing sight of the bigger picture, and understanding how political shifts can reshape industries, markets, and portfolios.

That is exactly what we do with GD Pro.

Every weekday, we provide succinct, high-value intelligence—modeled on the US President’s Daily Brief—to help investors and business leaders cut through the noise and stay ahead of market-moving geopolitical shifts.

On Saturdays, our Week Signals report examines the most significant geopolitical themes of the week, what they mean for business, and what to prepare for in the days ahead—giving you a strategic edge before Monday’s market opens.

And once a month, our private client roundtable provides an exclusive opportunity to engage directly with our senior advisors—many of whom are former ambassadors, diplomats, and global strategists. This is a forum to stress-test assumptions, discuss emerging risks, and identify opportunities before they are priced in. (Existing GD Pro subscribers can access the recording from our most recent webinar below.)

In today’s environment—jittery markets, unpredictable policymakers, and rising geopolitical risks—investors need a systematic approach to geopolitical intelligence. Subscribe to GD Pro today and gain the insights that help you anticipate risks before they become losses—and seize opportunities before they are priced in.

(For institutional investors and leadership teams, we also offer group subscriptions. Click here for details on discounted rates.)

Kind regards

Damien Bruckard

CEO, Geopolitical Strategy

GD Pro Webinar — February:

This post is for subscribers in the GD Corporate Membership plan

| A guest post by

|